Joint interest billing sits at the point where cost accounting, partner relationships, and operational discipline intersect. In upstream environments, platforms like Quorum’s My Quorum Accounting and Upstream On Demand Accounting connect JIB with broader financial workflows, but the outcome still depends on how well the underlying process is executed. The operator must gather costs, apply agreement terms, and issue partner billing that is both accurate and explainable.

Key Takeaway

JIB quality is determined upstream of the statement. Source transaction accuracy, consistent coding, ownership data, and agreement logic drive the result. The process must produce billing that partners can trace and understand without additional interpretation.

What Joint Interest Billing Covers

Joint interest billing allocates shared costs based on ownership interests and agreement terms. The operator incurs costs while managing the asset and distributes those costs to non-operating partners according to defined rules. These costs span drilling, completions, lease operating expenses, facilities work, overhead, and other categories permitted by the governing agreement.

The billing outcome depends on the condition of upstream inputs. Transactions must tie back to real operational or accounting activity, agreement rules must be applied consistently, and the resulting statements must be structured in a way partners can follow. Variability in joint operating agreements—such as differences in overhead treatment or exclusions—adds complexity that must be managed through disciplined data and coding practices.

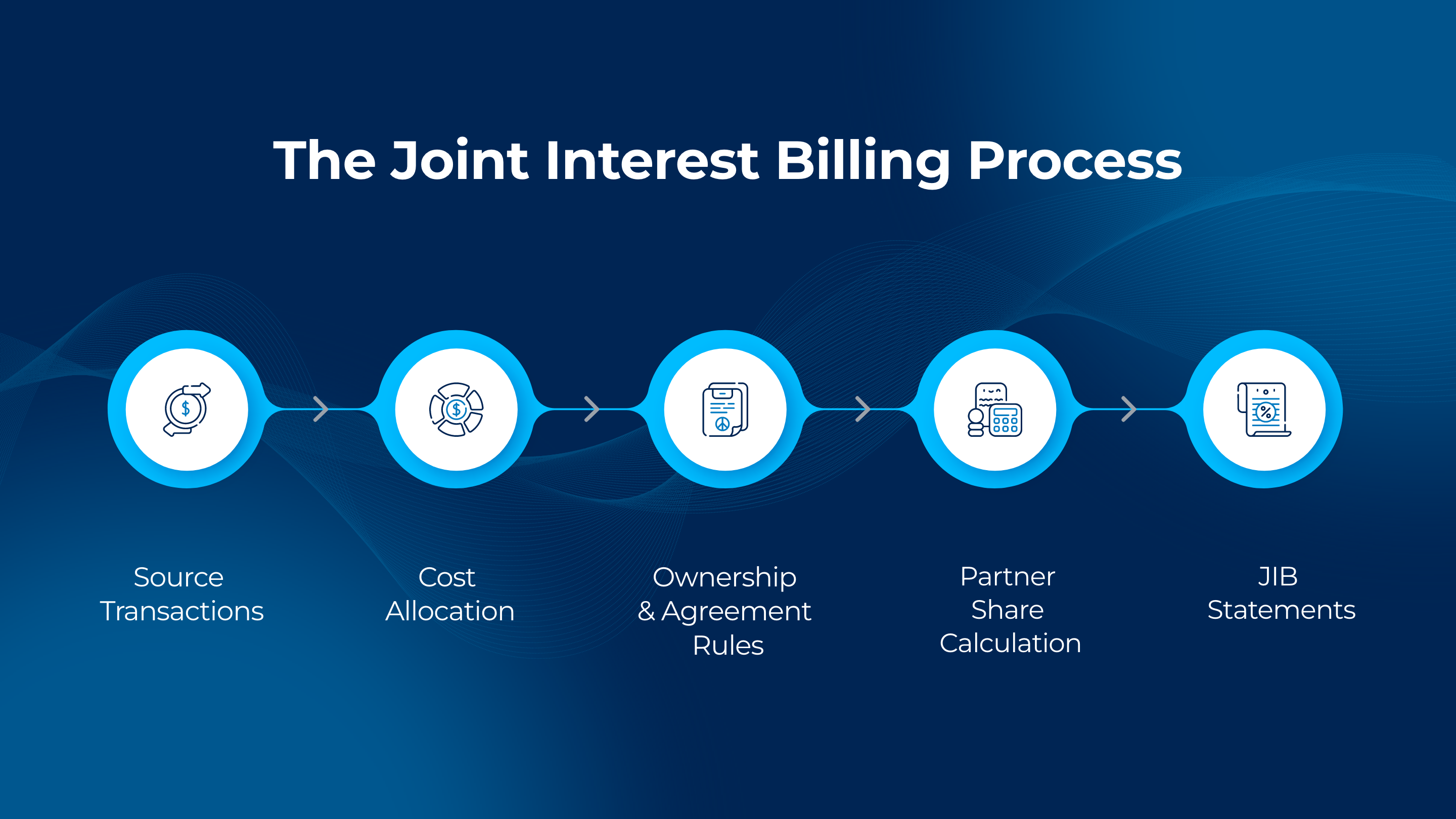

How the End-to-End Non-Op Billing Process Works

The workflow begins when source transactions enter the accounting environment from vendor invoices, field activity, payroll allocations, or internal charges. Each transaction is reviewed, coded, and assigned to the appropriate asset structure.

From there, the process moves through a defined sequence:

- Transactions are aligned to the correct properties, wells, and cost categories

- Ownership interests and effective dates are applied

- Agreement terms determine which costs are allocable

- Partner shares are calculated and billed

This sequence defines the integrity of the billing output. Errors introduced early—such as incorrect coding or ownership mismatches—carry through to the final statement. As transaction volume increases, consistency becomes more important than speed, because unclear billing creates downstream reconciliation effort.

Process Variability and Data Dependency

JIB depends on the quality and governance of upstream data. Ownership records, effective dates, and cost category mappings must be maintained consistently across properties and time periods.

Variability typically appears when ownership changes are not aligned to effective dates, when cost categories are applied inconsistently, or when agreement rules are interpreted differently across assets. When governance is structured, the billing output remains stable. When it is not, the same process produces inconsistent results that surface during reconciliation.

Where JIB Reconciliation Issues Come From

Most reconciliation issues fall into three categories:

| Reconciliation Issue Type | What Happens | How to Reduce It |

| Source data issue | Transactions are coded or allocated incorrectly before billing | Strengthen validation before billing and enforce coding standards |

| Interpretation issue | Partners cannot understand the category or rule applied | Use consistent statement formats and clearer supporting detail |

| Timing issue | Accruals or late invoices create period differences | Apply defined accrual logic and provide period visibility |

When issues arise, teams work backward through the process to determine whether the problem originated in source coding, agreement application, or timing. The speed of resolution depends on how clearly the billed amount can be traced to its origin.

Why Accuracy Alone Is Not Enough

A billing can be mathematically correct and still create unnecessary work. If supporting detail is difficult to follow, partners must interpret the charges manually, which introduces delays and increases the volume of questions.

Confidence comes from traceability. Each billed amount should connect directly to the source transaction, the applied agreement logic, and the ownership structure. Consistent statement formats across periods further reduce interpretation effort by making the billing predictable to review.

Role of Systems and Data

Systems enforce structure, but they depend on the quality of the data they manage. Ownership, agreement terms, and cost classifications must be governed consistently for the system to produce reliable results.

When systems and data are aligned, the process supports repeatable allocation, consistent statement generation, and visibility into exceptions. This reduces manual effort and improves auditability without changing the underlying workflow.

What a Scalable JIB Process Looks Like

A scalable JIB process maintains consistency across assets, partners, and billing cycles. It applies agreement rules without manual intervention and produces statements that partners can review without additional explanation.

This state is achieved through disciplined upstream control—accurate coding, governed ownership data, consistent allocation logic, and defined handling of timing differences. As volume increases, the process remains stable rather than generating additional reconciliation work.

Focusing on Upstream Data Quality and Agreement Governance

Joint interest billing reflects the full process from source transaction through allocation and partner communication. When each step is controlled and traceable, the billing becomes easier to produce, explain, and reconcile.

Organizations that focus on upstream data quality and agreement governance reduce disputes, improve partner confidence, and maintain a more predictable billing cycle.

Learn more about My Quorum Accounting or Upstream On Demand Accounting.

Frequently Asked Questions About Joint Interest Billing

What is JIB in oil and gas?

Joint interest billing is the process of allocating shared costs to partners based on ownership interests and joint operating agreement terms.

What is the difference between JIB and revenue distribution?

JIB handles cost allocation and billing, while revenue distribution allocates sales proceeds to partners. Both depend on ownership data but operate on different sides of the financial process.

How can operators reduce JIB disputes with non-operating partners?

Disputes are reduced by improving traceability and consistency through accurate coding, consistent agreement application, stable statement formats, and clear supporting detail.

Previous Page

Previous Page